![[Chronicle]](/images/sidebar_header_oct06.gif)

Vol. 28 No. 9

Financial implications of eroding trust

Study shows how trust has become powerful motivator for Americans’ financial decisions

By Allan Friedman

allan.friedman@chicagobooth.edu

Chicago Booth Communications

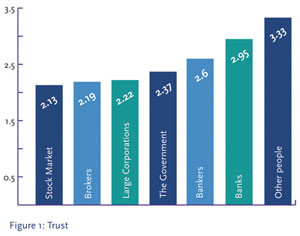

Average response on a scale from 1 to 5 to the question, “How much do you trust...” where 1 means “I do not trust at all” and 5 means “I trust completely.” |

|

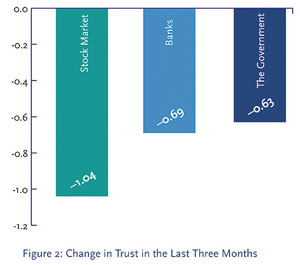

Average response to the question, “How has your trust in some of these institutions changed in the last three months?” “Would you say your trust in … has 1) Increased a lot; 2) Increased a little; 3) Decreased a little; 4) Decreased a lot; or 5) Has there been no change in your trust.” The scale was coded with 5 as 0, 3 as -1, 4 as -2, 1 as +2, and 2 as +1. |

|

As unemployment rates rise, the housing crisis deepens and 401Ks continue to deplete, it should come as no surprise that America’s trust in its financial leaders and institutions has plummeted.

To study the financial implications of eroding trust, Luigi Zingales, the Robert C. McCormack Professor of Entrepreneurship and Finance and the David G. Booth Faculty Fellow at Chicago Booth, and Paola Sapienza of the Kellogg School of Management, have created the Chicago Booth/Kellogg School Financial Trust Index. The accompanying research shows just how deep America’s declining trust runs and how strongly it contributes to the country’s financial problems.

“Trust is a powerful motivator of economic behavior,” said Sapienza. “Our previous research and anecdotal evidence suggest that lack of trust can have paralyzing effects on financing and investments. We developed the Financial Trust Index to measure this often ignored economic indicator and gain insight into how the government’s reaction affects the economy.”

The Financial Trust Index will measure public opinion every three months to track changes in attitude over time and will provide a better understanding of public trust, the absence of which, according to Sapienza and Zingales, can bring even the richest, most advanced economies to a grinding halt.

Seeking to formalize the relationship between trust and finance, Sapienza and Zingales analyzed data from more than 1,000 American households, randomly chosen and surveyed via phone over two weeks in late December 2008.

Sapienza and Zingales found that only 22 percent of those surveyed currently trust the financial system. Only 12 percent of people trust the stock market. This trust is a strong predictor of individuals’ intentions to increase or decrease their investment in the stock market over the next few months.

Similarly, they find that 11 percent of the respondents withdrew money from the bank and kept it in cash during the crisis. This behavior is highly correlated with individuals’ trust for banks.

They also found that trust in the financial sector has declined sharply over the last few months. When asked how their trust had changed over the past three months, respondents indicated a decrease across all categories, with perceptions of the stock market most soured.

One of the goals of this research was to determine to what extent, if any, the perception of current events and government policy impact the trust people have in financial markets.

Respondents who identify the main cause of the 2008 financial crisis as lax government oversight (16 percent) or regulation (15 percent) exhibit the least trust in the market. Levels of trust were also low among those who blamed companies, citing poor corporate governance (15 percent) or managerial greed (36 percent).

While the heavy financial losses suffered can, in part, explain this reduced trust, a crucial factor seems to be the way in which the government has intervened.

While the majority of respondents favor government intervention in financial markets, 80 percent said the way it intervened has made them less confident in the market. Even among the respondents who felt that federal intervention in the financial sector should increase, 75 percent still lost confidence as a result of recent federal intervention. This percentage rises to 95 percent among those who did not favor government intervention.

In other words, even among investors who are ideologically favorable to government intervention in financial markets, three out of four have been made less confident by the way the government has intervened.

“One of the key factors undermining trust,” said Zingales, “is the perception that the rules have changed in the middle of the game. The government has done exactly this. What is most shocking is how deeply this has affected the trust of the average American.”

Further questions proved that “coziness” between government and the financial industry, whether real or perceived, is clearly a problem in the eyes of many Americans. Respondents were asked to choose what motivated former Treasury Secretary Hank Paulson as he engineered and executed the government response. While 20 percent of respondents had no opinion, the remaining 80 percent were evenly split. Half the group, 40 percent of the overall respondents, believed Paulson acted in the interest of the country. The other 40 percent, however, believed that Paulson’s plan was meant to benefit Goldman Sachs, the investment bank at which he served as chairman and CEO prior to being appointed Secretary.

Social Science Research Solutions, using International Communications Research’s weekly telephone omnibus service, surveyed 1,034 individuals over two weeks, starting on Wednesday, Dec. 17, 2008. A fully replicated, stratified, single-stage random-digit-dialing sample of landline telephone households was used to identify survey subjects. Within each sample household, one adult respondent was randomly selected using a computerized procedure based on the “Most Recent Birthday Method” of respondent selection. Once a respondent was contacted, he or she was asked if they are the main or joint financial decision makers in the household. Only individuals replying positively to this question were surveyed.

To see the full study, visit http://igmchicago.org/trust.

Related links: http://www.chicagogsb.edu/faculty/bio.aspx?person_id=312062